SELF MANAGED SUPERFUND (SMSF)

Limited Recourse Loans

The information provided within this memorandum is general information only and provided as a guide to the steps involved in borrowing money and buying property through a Self-Managed Superannuation Fund (SMSF). This information is not legal or financial advice and you should obtain professional legal, financial and taxation advice before applying for any loan or purchasing any property through your SMSF.

SELF MANAGED SUPERFUND (SMSF)

Limited Recourse Loans

The information provided within this memorandum is general information only and provided as a guide to the steps involved in borrowing money and buying property through a Self-Managed Superannuation Fund (SMSF). This information is not legal or financial advice and you should obtain professional legal, financial and taxation advice before applying for any loan or purchasing any property through your SMSF.

TABLE OF CONTENTS

Introduction

Basic Structure

How Does It All Work?

The Loan

The Legal Structure

1

INTRODUCTION

Prior to 2007, the SIS (Superannuation Industry Supervision) Act 1993 prohibited a Self-Managed Superannuation Fund (referred to as a ‘Super Fund’ in this document), from borrowing money to purchase assets. Amendments to the SIS Act were introduced to allow Super Fund’s to invest in any kind of asset and to borrow, charging those assets so long as there is no recourse for the borrowing against the Super Fund.

New section’s 67A & 67B of the SIS Act permit a Super Fund to borrow money if:

(a) the money borrowed is applied for the purchase of an asset;

(b) the asset is held on trust so that the Super Fund acquires a beneficial interest;

(c) the Super Fund has the right to acquire legal ownership by making payment;

(d) the rights of the lender against the Super Fund for default are limited to the security.

2

BASIC STRUCTURE

The Super Fund can only borrow money to purchase an asset if it complies with the following:

The Super Fund may select any property, residential or commercial. The purchase must be an ‘arm’s length transaction’ (i.e. the property is purchased from a ‘stranger’). There is an exception for ‘business assets’ (i.e. property leased to a tenant who conducts a business in the property). In this case, the property may be purchased from a ‘related party’ of the Super Fund.

The legal title to the property must be held on trust by an independent trustee.

The beneficial title to the property will be held by the Super Fund.

The lenders recourse will be limited to the property, thereby providing the Super Fund absolute protection for its other assets). Certain lenders will also require a personal guarantee from all members of the Super Fund.

All rents will be paid directly to the Super Fund.

The Super Fund will make loan repayments to the lender.

Super Funds can deal with the property however and whenever they like, in the same way as you can deal with ‘normal’ investment properties (e.g. lease, repair, or sell).

The Super Fund can pay out or reduce the mortgage at any time (subject to the terms of the relevant loan).

When the mortgage is paid out in full, title to the property may be transferred to the Super Fund by the Property Trustee, or the Property Trustee may continue as registered proprietor.

It is important that the structure clearly complies with all the above requirements. Failure to do so may result in the Super Fund being declared ‘non-compliant’ within the meaning of the SIS Act.

It is also important to adhere to the lenders varying trustee requirements when establishing the legal structure. For example, certain lenders require a corporate trustee for the Super Fund, whilst the others will allow individual trustees.

3

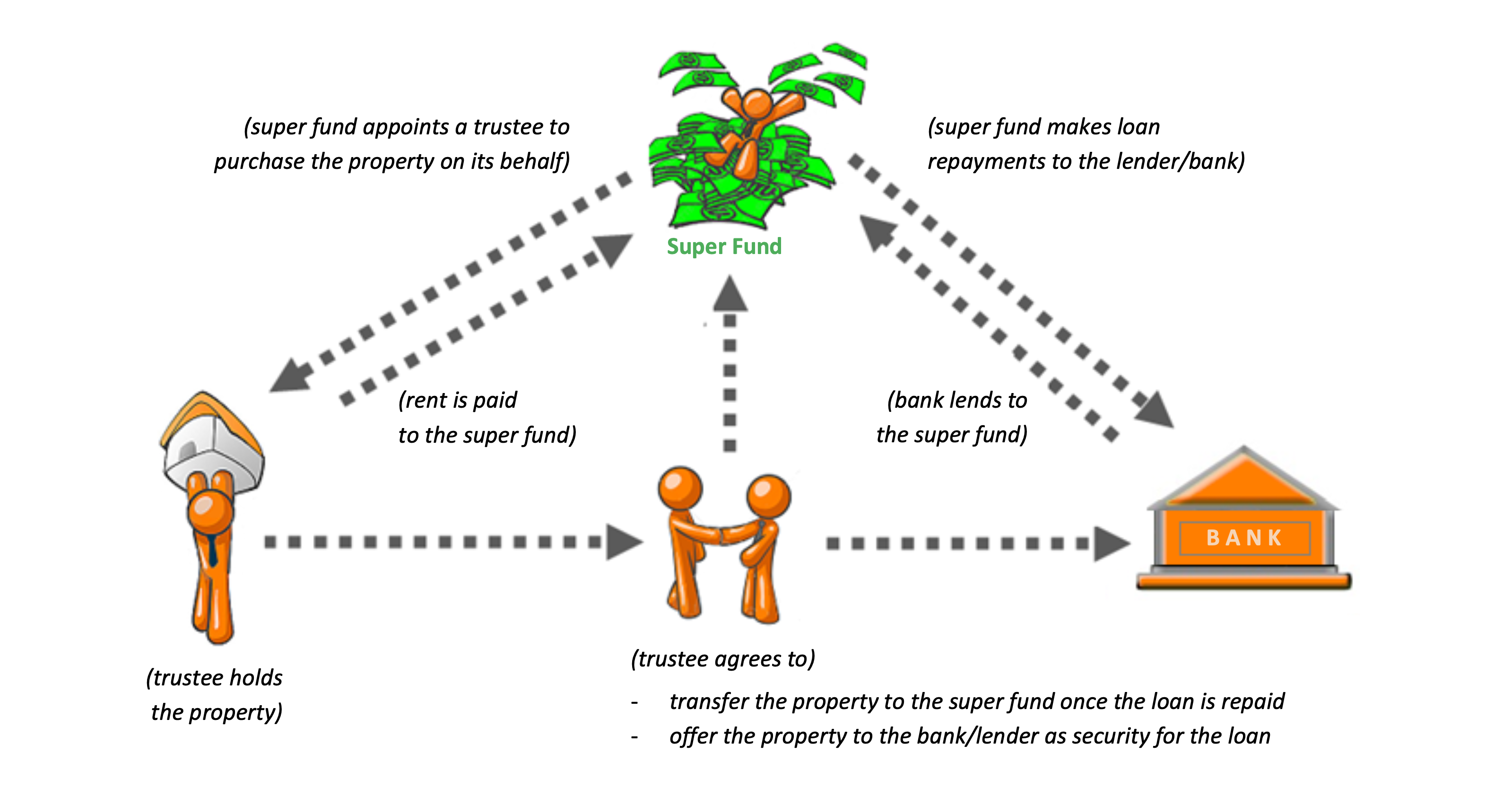

HOW DOES IT ALL WORK?

There are several entities that complete the purchase/borrowing structure, the diagram below illustrates each including their duties & responsibilities.

4

THE LOAN

It's an ordinary loan that enables you to purchase residential or commercial property with the Super Fund paying the deposit and any other cost/s, i.e. stamp duty;

Complies with the Government Legislation (SIS Act - s67A, 67B);

It is a ‘Limited Recourse Loan’, meaning the lender cannot touch any other Super Fund assets other than the property held as security.

Loan products are restricted by nature and typically limited to:

A variable rate loan; or

A fixed rate loan, 1-5 years.

What other restrictions are there?

It is important to remember that there are loan restrictions associated with this borrowing arrangement:

Loan term on refinance of the loan restricted to the remaining loan term of initial loan;

No increase in the loan amount post settlement;

All Super Fund property purchasers must be on a ‘stand alone’ basis, no other assets inside or outside the Super Fund can be utilised.

5

THE LEGAL STRUCTURE

In order for a Super Fund to purchase an investment property and borrow money, it will be necessary to have a special legal structure in place.

Property/Bare Trust Deed

The Property/Bare Trust Deed is a key component within the legal structure and extreme care is required so to ensure there are no adverse GST, taxation or stamp duty consequences.

The SIS Act requires where an asset is acquired with the proceeds from a loan, the asset "is held on trust” with the Super Fund being the beneficial owner to the asset at all times. Once the loan is repaid in full the asset can then be transferred to the Super Fund.

Superfund’s Trust Deed

The Super Fund’s Trust Deed contains the rules that govern the Super Fund. This being the case, the Trustee of the Fund must ensure that the Trust Deed contains all of the provisions required under the section 67(A&B) of the SIS Act.

TABLE OF CONTENTS

Introduction

Basic Structure

How Does It All Work?

The Loan

The Legal Structure

1

INTRODUCTION

Prior to 2007, the SIS (Superannuation Industry Supervision) Act 1993 prohibited a Self-Managed Superannuation Fund (referred to as a ‘Super Fund’ in this document), from borrowing money to purchase assets. Amendments to the SIS Act were introduced to allow Super Fund’s to invest in any kind of asset and to borrow, charging those assets so long as there is no recourse for the borrowing against the Super Fund.

New section’s 67A & 67B of the SIS Act permit a Super Fund to borrow money if:

(a) the money borrowed is applied for the purchase of an asset;

(b) the asset is held on trust so that the Super Fund acquires a beneficial interest;

(c) the Super Fund has the right to acquire legal ownership by making payment;

(d) the rights of the lender against the Super Fund for default are limited to the security.

2

BASIC STRUCTURE

The Super Fund can only borrow money to purchase an asset if it complies with the following:

The Super Fund may select any property, residential or commercial. The purchase must be an ‘arm’s length transaction’ (i.e. the property is purchased from a ‘stranger’). There is an exception for ‘business assets’ (i.e. property leased to a tenant who conducts a business in the property). In this case, the property may be purchased from a ‘related party’ of the Super Fund.

The legal title to the property must be held on trust by an independent trustee.

The beneficial title to the property will be held by the Super Fund.

The lenders recourse will be limited to the property, thereby providing the Super Fund absolute protection for its other assets). Certain lenders will also require a personal guarantee from all members of the Super Fund.

All rents will be paid directly to the Super Fund.

The Super Fund will make loan repayments to the lender.

Super Funds can deal with the property however and whenever they like, in the same way as you can deal with ‘normal’ investment properties (e.g. lease, repair, or sell).

The Super Fund can pay out or reduce the mortgage at any time (subject to the terms of the relevant loan).

When the mortgage is paid out in full, title to the property may be transferred to the Super Fund by the Property Trustee, or the Property Trustee may continue as registered proprietor.

It is important that the structure clearly complies with all the above requirements. Failure to do so may result in the Super Fund being declared ‘non-compliant’ within the meaning of the SIS Act.

It is also important to adhere to the lenders varying trustee requirements when establishing the legal structure. For example, certain lenders require a corporate trustee for the Super Fund, whilst the others will allow individual trustees.

3

HOW DOES IT ALL WORK?

There are several entities that complete the purchase/borrowing structure, the diagram below illustrates each including their duties & responsibilities.

4

THE LOAN

It's an ordinary loan that enables you to purchase residential or commercial property with the Super Fund paying the deposit and any other cost/s, i.e. stamp duty;

Complies with the Government Legislation (SIS Act - s67A, 67B);

It is a ‘Limited Recourse Loan’, meaning the lender cannot touch any other Super Fund assets other than the property held as security.

Loan products are restricted by nature and typically limited to:

A variable rate loan; or

A fixed rate loan, 1-5 years.

What other restrictions are there?

It is important to remember that there are loan restrictions associated with this borrowing arrangement:

Loan term on refinance of the loan restricted to the remaining loan term of initial loan;

No increase in the loan amount post settlement;

All Super Fund property purchasers must be on a ‘stand alone’ basis, no other assets inside or outside the Super Fund can be utilised.

5

THE LEGAL STRUCTURE

In order for a Super Fund to purchase an investment property and borrow money, it will be necessary to have a special legal structure in place.

Property/Bare Trust Deed

The Property/Bare Trust Deed is a key component within the legal structure and extreme care is required so to ensure there are no adverse GST, taxation or stamp duty consequences.

The SIS Act requires where an asset is acquired with the proceeds from a loan, the asset "is held on trust” with the Super Fund being the beneficial owner to the asset at all times. Once the loan is repaid in full the asset can then be transferred to the Super Fund.

Superfund’s Trust Deed

The Super Fund’s Trust Deed contains the rules that govern the Super Fund. This being the case, the Trustee of the Fund must ensure that the Trust Deed contains all of the provisions required under the section 67(A&B) of the SIS Act.

Supplier to National Tax & Accountants Association (NTAA) & CPA Members since 2007

Supplier to National Tax & Accountants Association (NTAA) & CPA Members since 2007

Privacy Policy | Terms of Service

© 2007 LRBA Structures | All rights reserved.

Privacy Policy | Terms of Service